If you have ever been caught off-guard by a large medical bill, a long-running practice known as balance billing might be the reason. A balance bill — which is the difference between an out-of-network provider’s normal charges for a service and a lower rate reimbursed by insurance — can amount to thousands of dollars.

Many consumers are already aware that it usually costs less to seek care from in-network health providers, but that’s not always possible in an emergency. Complicating matters, some hospitals and urgent-care facilities rely on physicians, ambulances, and laboratories that are not in the same network. In fact, a recent survey found that 18% of emergency room visits resulted in at least one surprise bill.1

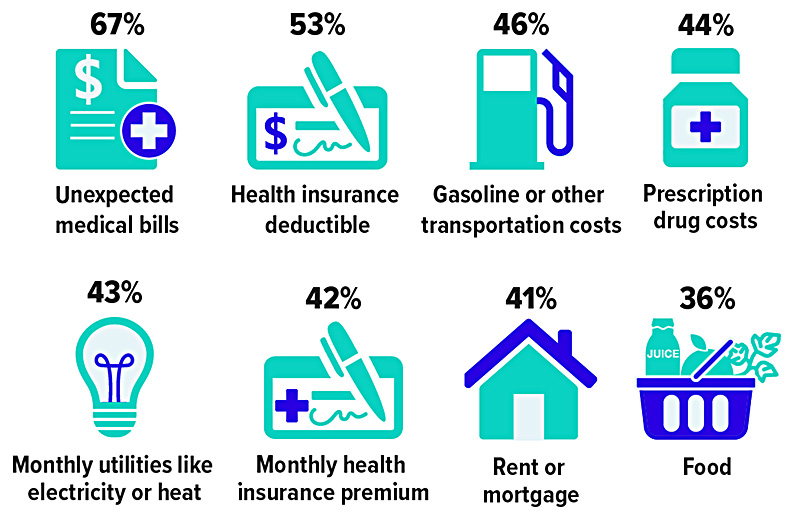

Who’s Afraid of High Health-Care Costs? Most People

Percent of surveyed adults who say they are worried about being able to afford the following expenses

Coming Soon: Comprehensive Protection

The No Surprises Act was included in the omnibus spending bill enacted by the federal government at the end of 2020. The new rules will help ensure that consumers do not receive unexpected bills from out-of-network providers they didn’t choose or had no control over. Once the new law takes effect in 2022, patients will not receive balance bills for emergency care, or for nonemergency care at in-network hospitals, when they are unknowingly treated by out-of-network providers. (A few states already have laws that prevent balance billing unless the patient agrees to costlier out-of-network care ahead of time.)

Patients will be responsible only for the deductibles and copayment amounts that they would owe under the in-network terms of their insurance plans. Instead of charging patients, health providers will negotiate a fair price with insurers (and settle disputes with arbitration). This change applies to doctors, hospitals, and air ambulances — but not ground ambulances.

Consent to Pay More

Some patients purposely seek care from out-of-network health providers, such as a trusted family physician or a highly regarded specialist, when they believe the quality of care is worth the extra cost. In these nonemergency situations, physicians can still balance bill their patients. However, a good-faith cost estimate must be provided, and a consent form must be signed by the patient, at least 72 hours before treatment. Some types of providers are barred from seeking consent to balance bill for their services, including anesthesiologists, radiologists, pathologists, neonatologists, assistant surgeons, and laboratories.

Big Bills Will Keep Coming

The fact that millions of consumers could be saved from surprise medical bills is something to celebrate. Still, many people may struggle to cover their out-of-pocket health expenses, in some cases because they are uninsured, or simply due to high plan deductibles or rising costs in general. Covered workers enrolled in family coverage contributed $5,588, on average, toward the cost of premiums in 2020, with deductibles ranging from $2,700 to more than $4,500, depending on the type of plan.2

When arranging nonemergency surgery or other costly treatment, you may want to take your time choosing a doctor and a facility because charges can vary widely. Don’t hesitate to ask for detailed estimates and try to negotiate a better price.

If you receive a bill that is higher than expected, don’t assume it is set in stone. Check hospital bills closely for errors, check billing codes, and dispute charges that you think insurance should cover. If all else fails, offer to settle your account at a discount.1-2) Kaiser Family Foundation, 2020

Prepared by Broadridge Advisor Solutions Copyright 2022.

HENRY is a catchy acronym for “high earner, not rich yet.” It describes a demographic made up of young and often highly educated professionals with substantial incomes but little or no savings. HENRYs generally have enviable career prospects, but many of them feel financially stretched or may even live paycheck to paycheck for years, especially if they are working in cities with high living costs and/or facing large student loan payments.

If this sounds like you, it may be time to shed your HENRY status for good and focus on growing wealth — even if it means making some temporary sacrifices. One simple metric that can be used to gauge your financial standing is your net worth, which is the total of your assets (what you own) minus your liabilities (what you owe).

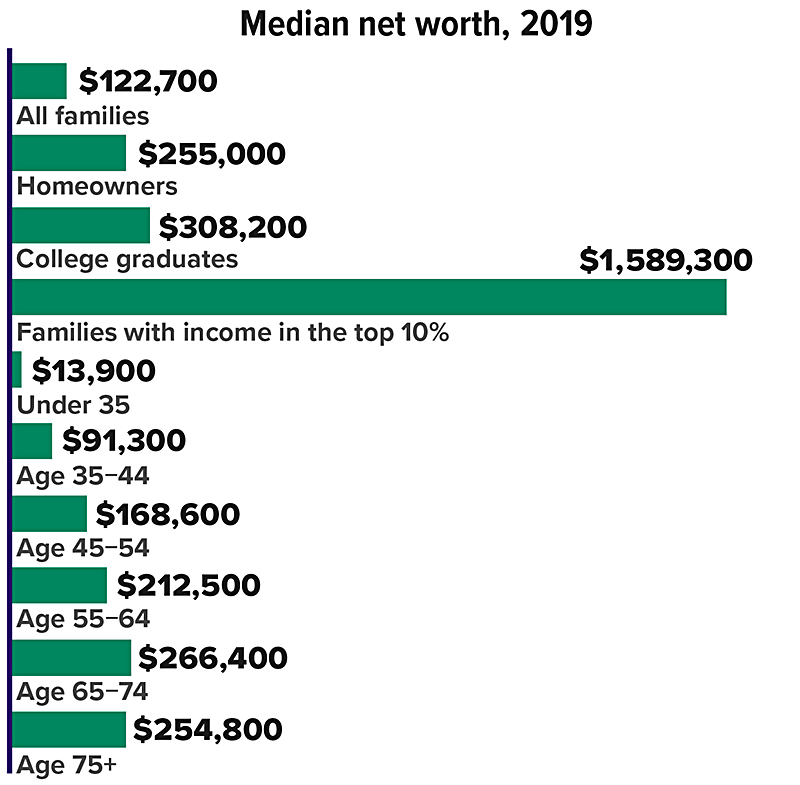

Wealth Snapshot

The net worth of U.S. families varies greatly depending on housing status, education, and income level. But it also takes time to build wealth, so there are significant differences by age.

Pay Attention to Your Spending

It’s virtually impossible to increase your net worth if you don’t live within your means. After studying long hours and working your way into a good-paying job, you may feel that you deserve to spend some money on fashionable clothes, the latest smartphone, a night on the town, or a relaxing vacation. However, if you can’t pay for most of your splurges without relying on credit — or wiping out your savings — then you may need to rein in your lifestyle. Budgeting software and/or smartphone apps can help you analyze your spending patterns and track your financial progress.

Utilize a Workplace Retirement Plan

Making regular pre-tax contributions to a traditional 401(k) plan is a no-nonsense way to accumulate retirement assets, and it helps reduce your taxable income by the same amount. Experts recommend saving at least 10% of your income for future needs, but if that’s not possible right away, start by contributing 3% to 6% of your salary to your retirement plan and elect to escalate your contribution level by 1% each year until you reach your target (or the contribution limit). The maximum you can contribute to a 401(k) plan in 2022 is $20,500 ($27,000 if you are age 50 or older).

Many companies will match part of employee contributions, and free money is a great reason to save at least enough to receive a full company match and any available profit sharing. Some plans may require that you remain employed by the company for a certain amount of time before you can keep the matching funds.

Assess Your Housing Situation

Paying rent indefinitely may do little to improve your financial situation. Buying a home with a fixed-rate mortgage could help stabilize your housing costs, and you can build equity in the property over time as your loan balance is paid off — especially if the value appreciates. A home purchase may also afford tax advantages, but only if you itemize rather than claim the standard deduction on your tax return. Interest paid on up to $750,000 of mortgage loan debt is deductible, as are the property taxes, subject to a $10,000 cap on state and local property taxes.

Homeownership is a worthwhile financial goal if you plan to stay put for at least several years. And in many places, owning a home can be less expensive than renting, thanks to low interest rates. But there could be hurdles to overcome, including a hot real estate market, high prices, lingering student debt, and the large chunk of money required for a down payment.

When shopping for a home, resist the temptation to buy more house than you can afford, even if the bank says you can. And don’t forget to factor property taxes, insurance, and potential maintenance costs into your buying decisions and household budget.

Prepared by Broadridge Advisor Solutions Copyright 2022.

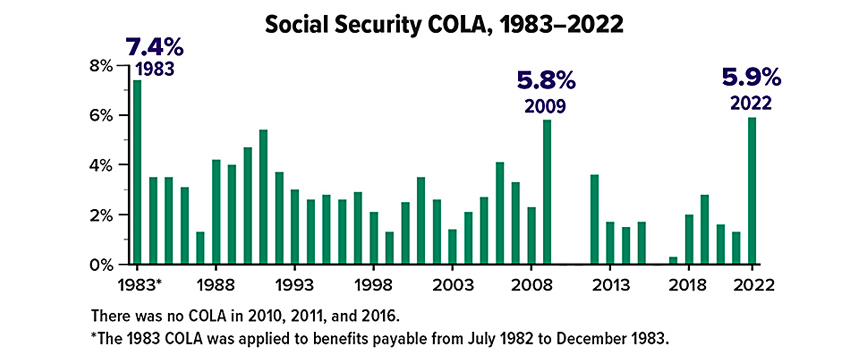

The Social Security cost-of-living adjustment (COLA) for 2022 is 5.9%, the largest increase since 1983. The COLA applies to December 2021 benefits, payable in January 2022. The amount is based on the increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from Q3 of the last year a COLA was determined to Q3 of the current year (in this case, Q3 2020 to Q3 2021).

Despite these annual adjustments for inflation, a recent study found that the buying power of Social Security benefits declined by 30% from 2000 to early 2021, in part because the CPI-W is weighted more heavily toward items purchased by younger workers than by Social Security beneficiaries.

Sources: Social Security Administration, 2021; The Senior Citizens League, August 11, 2021

Prepared by Broadridge Advisor Solutions Copyright 2022.

Although scammers often target older people, younger people who encounter scams are more likely to lose money to fraud, perhaps because they have less financial experience. When older people do fall for a scam, however, they tend to have higher losses.1

Regardless of your age or financial knowledge, you can be certain that criminals are hatching schemes to separate you from your money — and you should be especially vigilant in cyberspace. In a financial industry study, people who encountered scams through social media or a website were much more likely to engage with the scammer and lose money than those who were contacted by telephone, regular mail, or email.2

Here are four common practices that may help you identify a scam and avoid becoming a victim.3

Scammers pretend to be from an organization you know. They might claim to be from the IRS, the Social Security Administration, or a well-known agency or business. The IRS will never contact you by phone asking for money, and the Social Security Administration will never call to ask for your Social Security number or threaten your benefits. If you wonder whether a suspicious contact might be legitimate, contact the agency or business through a known number. Never provide personal or financial information in response to an unexpected contact.

Scammers present a problem or a prize. They might say you owe money, there’s a problem with an account, a virus on your computer, an emergency in your family, or that you won money but have to pay a fee to receive it. If you aren’t aware of owing money, you probably don’t. If you didn’t enter a contest, you can’t win a prize — and you wouldn’t have to pay for it if you did. If you are concerned about your account, call the financial institution directly. Computer problems? Contact the appropriate technical support. If your “grandchild” or other “relative” calls asking for help, ask questions only the grandchild/relative would know and check with other family members.

Scammers pressure you to act immediately. They might say you will “miss out” on a great opportunity or be “in trouble” if you don’t act now. Disengage immediately if you feel any pressure. A legitimate business will give you time to make a decision.

Scammers tell you to pay in a specific way. They may want you to send money through a wire transfer service or put funds on a gift card. Or they may send you a fake check, tell you to deposit it, and send them money. By the time you discover the check was fake, your money is gone. Never wire money or send a gift card to someone you don’t know — it’s like sending cash. And never pay money to receive money.

For more information, visit consumer.ftc.gov/features/scam-alerts.1, 3) Federal Trade Commission, 2020

2) FINRA Investor Education Foundation, 2019

Prepared by Broadridge Advisor Solutions Copyright 2021.

As the beneficiary of an inheritance, you are most likely to be faced with making many important decisions during an emotional time. Short of meeting any required tax or legal deadlines, don’t make any hasty decisions concerning your inheritance.

Identify a Team of Trusted Professionals

Tax laws and requirements can be complicated. Consult with professionals who are familiar with assets that transfer at death. These professionals may include an attorney, an accountant, and a financial and/or insurance professional.

Be Aware of the Tax Consequences

Generally, you probably will not owe income tax on assets you inherit. However, your income tax liability may eventually increase. Any income that is generated by inherited assets may be subject to income tax, and if those assets produce a substantial amount of income, your tax bracket may increase. This is particularly true if you receive distributions from a tax-qualified retirement plan such as a 401(k) or an IRA. You may need to re-evaluate your income tax withholding or begin paying estimated tax.

You also may need to consider the amount of potential transfer (estate) taxes that your estate may owe, due to the increase in the size of your estate after factoring in your inheritance. You may need to consider ways to help reduce these potential taxes.

How You Inherit Assets Makes a Difference

Your inheritance may be received through a trust or you may inherit assets outright. When you inherit through a trust, you’ll receive distributions according to the terms of the trust. You may not have total control over your inheritance as you would if you inherited the assets outright.

Familiarize yourself with the trust document and the terms under which you are to receive trust distributions. You will have to communicate with the trustee of the trust, who is responsible for the administration of the trust and the distribution of assets according to the terms of the trust.

Even if you’re used to handling your own finances, receiving a significant inheritance may promote spending without planning. Although you may want to quit your job, or buy a car, a house, or luxury items, this may not be in your best interest. Consider your future needs, as well, if you want your wealth to last. It’s a good idea to wait at least a few months after inheriting money to formulate a financial plan. You’ll want to consider your current lifestyle and your future goals, formulate a financial strategy to meet those goals, and determine how taxes may reduce your estate.

Develop a Financial Plan

Once you have determined the value and type of assets you will inherit, consider how those assets will fit into your financial plan. For example, in the short term, you may want to pay off consumer debt such as high-interest loans or credit cards. Your long-term planning needs and goals may be more complex. You may want to fund your child’s college education, put more money into a retirement account, invest, plan to help reduce taxes, or travel.

Evaluate Your Insurance Needs

Depending on the type of assets you inherit, your insurance needs may need to be adjusted. For instance, if you inherit valuable personal property, you may need to adjust your property and casualty insurance coverage. Your additional wealth from your inheritance means you probably have more to lose in the event of a lawsuit. You may want to purchase an umbrella liability policy that can help protect you against actual loss, large judgments, and the cost of legal representation. You may also need to recalculate the amount of life insurance you need because of your inheritance. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased.

Evaluate Your Estate Plan

Depending on the value of your inheritance, it may be appropriate to re-evaluate your estate plan. Estate planning involves conserving your money and putting it to work so that it best fulfills your goals. It also means helping reduce your exposure to potential taxes and creating a comfortable financial future for your family and other intended beneficiaries.

Some things you should consider are to whom your estate will be distributed, whether the beneficiary(ies) of your estate are capable of managing the inheritance on their own, and how you can best shield your estate from estate taxes. If you have minor children, you may want to protect them from asset mismanagement by nominating an appropriate guardian or setting up a trust for them. If you have a will, your inheritance may make it necessary to make significant changes to that document, or you may want to make an entirely new will or trust. There are costs and ongoing expenses associated with the creation and maintenance of trusts and wills. Consult with an estate planning attorney for proper guidance.

Prepared by Broadridge Advisor Solutions Copyright 2021.