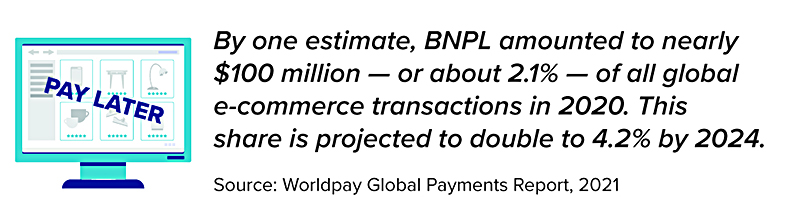

If you shop online, you might have noticed a growing number of buy now, pay later (BNPL) services that offer the option to spread out the payments on your purchases. Buyers who make one partial payment upfront and agree to several additional interest-free installments can receive their orders right away. This is a key difference from the layaway plans of the past: Shoppers had to wait until the balance was paid to take their goods home. Many stores discontinued layaway plans in the 1980s when the use of credit cards became widespread.

BNPL plans are more popular with younger consumers trying to stretch their paychecks, partly because they are more comfortable shopping online (and particularly on smartphones). At first glance, it may seem like a worthwhile convenience, but there are good reasons to think twice before committing to installment purchases.

Credit Is Credit

BNPL plans are essentially point-of-sale loans. Applying for the financing is quick and easy, which seems like a plus when time is tight.

However, speedy access to credit also provides instant gratification and allows for more impulse buying. It might tempt you to overspend on things you don’t really need and probably wouldn’t buy if you had to save up and/or pay 100% of the cost upfront. And if you make a lot of smaller purchases across multiple services, it may be harder to keep track of how much you are actually spending.

In fact, one criticism of BNPL services is that they make it easier for consumers to fall into debt. As with credit cards, you would face financial consequences such as late fees and/or high interest rates if you encounter a financial setback and can’t pay the installments on schedule.

Another point to consider is that credit-card companies report on-time payments to the credit bureaus, so using credit cards responsibly can help you build a positive credit history. In contrast, some BNPL lenders may not bother to report on-time payments — though they will surely report missed payments and collections. Before you use any BNPL service, read the fine print carefully to make sure you understand the terms and conditions and the company’s credit reporting policies.

Prepared by Broadridge Advisor Solutions Copyright 2022.

Every year, the Internal Revenue Service announces cost-of-living adjustments that affect contribution limits for retirement plans and various tax deduction, exclusion, exemption, and threshold amounts. Here are a few of the key adjustments for 2022.

Estate, Gift, and Generation-Skipping Transfer Tax

- The annual gift tax exclusion (and annual generation-skipping transfer tax exclusion) for 2022 is $16,000, up from $15,000 in 2021.

- The gift and estate tax basic exclusion amount (and generation-skipping transfer tax exemption) for 2022 is $12,060,000, up from $11,700,000 in 2021.

Standard Deduction

Taxpayers can generally choose to itemize certain deductions or claim a standard deduction on their federal income tax returns. In 2022, the standard deduction is:

- $12,950 (up from $12,550 in 2021) for single filers or married individuals filing separate returns

- $25,900 (up from $25,100 in 2021) for married joint filers

- $19,400 (up from $18,800 in 2021) for heads of household

The additional standard deduction amount for the blind and those age 65 or older in 2022 is:

- $1,750 (up from $1,700 in 2021) for single filers and heads of household

- $1,400 (up from $1,350 in 2021) for all other filing statuses

Special rules apply for those who can be claimed as a dependent by another taxpayer.

IRAs

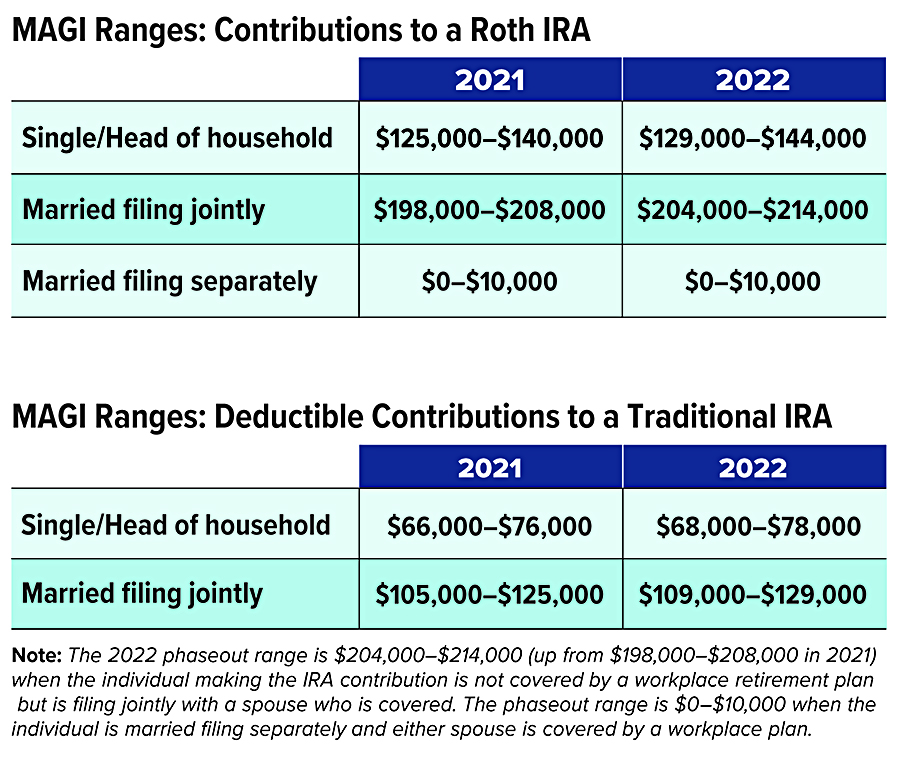

The combined annual limit on contributions to traditional and Roth IRAs is $6,000 in 2022 (the same as in 2021), with individuals age 50 or older able to contribute an additional $1,000. The limit on contributions to a Roth IRA phases out for certain modified adjusted gross income (MAGI) ranges (see chart). For individuals who are covered by a workplace retirement plan, the deduction for contributions to a traditional IRA also phases out for certain MAGI ranges (see chart). The limit on nondeductible contributions to a traditional IRA is not subject to phaseout based on MAGI.

Employer Retirement Plans

- Employees who participate in 401(k), 403(b), and most 457 plans can defer up to $20,500 in compensation in 2022 (up from $19,500 in 2021); employees age 50 or older can defer up to an additional $6,500 in 2022 (the same as in 2021).

- Employees participating in a SIMPLE retirement plan can defer up to $14,000 in 2022 (up from $13,500 in 2021), and employees age 50 or older can defer up to an additional $3,000 in 2022 (the same as in 2021).

Kiddie Tax: Child’s Unearned Income

Under the kiddie tax, a child’s unearned income above $2,300 in 2022 (up from $2,200 in 2021) is taxed using the parents’ tax rates.

Prepared by Broadridge Advisor Solutions Copyright 2022.

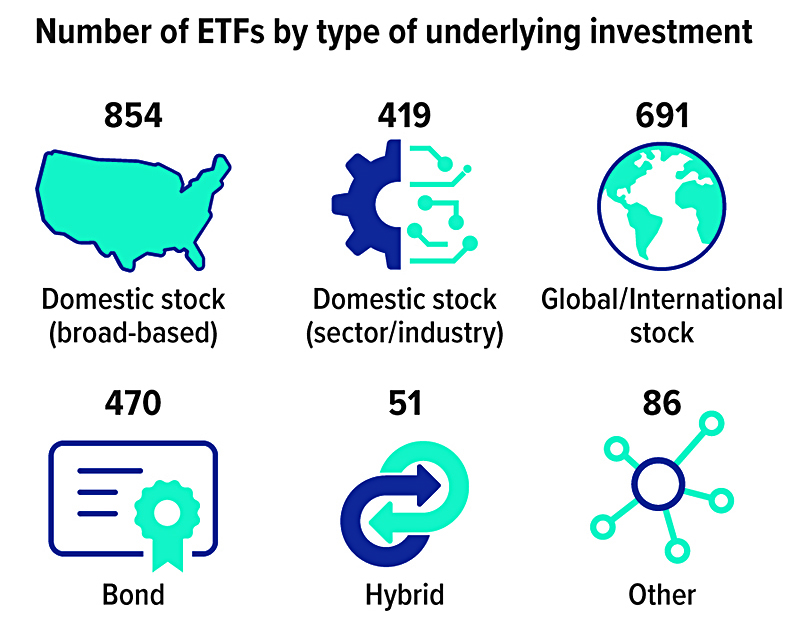

Investor demand for exchange-traded funds (ETFs) has increased over the last decade due to some attractive features that set them apart from mutual funds. In December 2021, almost $7.2 trillion was invested in more than 2,500 ETFs. This is equivalent to 27% of the assets invested in mutual funds, up from just 9% in 2011.1

Fund Meets Stock

Like a mutual fund, an ETF is a portfolio of securities assembled by an investment company. Mutual fund shares are typically purchased from and sold back to the investment company and priced at the end of the trading day, with the price determined by the net asset value (NAV) of the underlying securities. By contrast, ETF shares can be traded throughout the day on stock exchanges, like individual stocks, and the price may be higher or lower than the NAV because of supply and demand. In volatile markets, ETF prices may quickly reflect changes in market sentiment, while NAVs — adjusted once a day — take longer to react, resulting in ETFs trading at a premium or a discount.

Indexes and Diversification

Like mutual funds, ETFs may be passively managed, meaning they track an index of securities, or actively managed, guided by managers who assemble investments chosen to meet the fund’s objectives. Whereas active management is common among mutual funds, most ETFs are passively managed.

Investors can choose from a wide variety of indexes, ranging from broad-based stock or bond indexes to specific market sectors or indexes that emphasize certain factors. This makes ETFs a helpful tool to gain exposure to various market segments, investing styles, or strategies, potentially at a lower cost. Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss.

Tax Efficiency

Investors who own mutual fund shares actually own shares in the underlying investments, so when investments are sold within the fund, there may be capital gains taxes if the fund is held outside of a tax-advantaged account. By contrast, an investor who owns ETF shares does not own the underlying investments and generally will be liable for capital gains taxes only when selling the ETF shares.

Trading, Expenses, and Risks

ETFs typically have lower expense ratios than mutual funds — a large part of their appeal. However, you may pay a brokerage commission when you buy or sell shares, so your overall costs could be higher, especially if you trade frequently. Whereas mutual fund assets can usually be exchanged within a fund family at the end of the trading day at no cost, moving assets between ETFs requires selling and buying assets separately, which may be subject to brokerage fees and market shifts between transactions.

Plenty of Choices

Mutual funds typically have minimum investment amounts, but you can generally invest any dollar amount after the initial purchase, buying partial shares as necessary. By contrast, you can purchase a single share of an ETF if you wish, but you can typically only purchase whole shares.

The trading flexibility of ETFs may add to their appeal, but it could lead some investors to trade more often than might be appropriate for their situations. The principal value of ETFs and mutual funds fluctuates with market conditions. Shares, when sold, may be worth more or less than their original cost. The performance of an unmanaged index is not indicative of the performance of any specific security. Individuals cannot invest directly in any index.

Exchange-traded funds and mutual funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.1) Investment Company Institute, 2022

Prepared by Broadridge Advisor Solutions Copyright 2022.

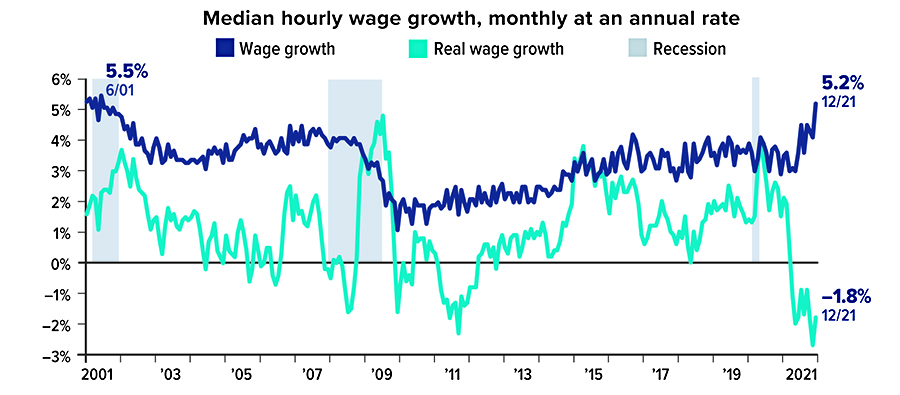

Driven by labor shortages, median hourly wages increased at an annual rate of 5.2% in December 2021, the highest level since June 2001. However, inflation cuts into buying power, and real wages — adjusted for inflation — actually dropped as inflation spiked in 2021. By contrast, negative inflation (deflation) during the Great Recession sent real wages skyrocketing temporarily even as non-adjusted wage growth declined.

Sources: Federal Reserve Bank of Atlanta, 2022, and U.S. Bureau of Labor Statistics, 2022, data 1/2001 to 12/2021. (Wage growth is calculated by comparing the median percentage change in wages reported by individuals 12 months apart; real wage growth is calculated by subtracting CPI-U inflation from wage growth.)

Prepared by Broadridge Advisor Solutions Copyright 2022.

It is widely recognized that financial literacy impacts a person’s overall economic success. In fact, studies have shown that individuals who are exposed to economic and financial education at an early age are more likely to exhibit positive financial behaviors when they are older (e.g., maintaining high credit scores, accumulating wealth). As a result, many states are requiring high school students to take a course in either economics or personal finance before they graduate.1

Whether you are just starting out and beginning to manage your own finances or simply want to stay on top of your current financial situation, it’s important to always keep these basic principles of financial literacy in mind.

1. Create a budget and stick with it. A budget helps you stay on track with your finances. Start by identifying your income and expenses. Next, compare the two totals to make sure you are spending less than you earn. Hopefully, your budget is still on the right track. If you find that your expenses outweigh your income, you’ll need to make some adjustments. Finally, while straying from your budget from time to time is normal, once you have a solid budget in place it’s important to try to stick with it.

2. Set financial goals. Setting goals is an important part of life, particularly when it comes to your finances. Short-term goals may include saving for a new car or building an emergency fund, while long-term goals may take more time to achieve (e.g., saving for a child’s education or retirement). Over time, your personal or financial circumstances will most likely change, so you’ll need to be ready to make adjustments and reprioritize your goals as needed.

3. Manage your credit and debt. Reducing debt is part of any healthy financial plan. Whether you have student loan debt, an auto loan, and/or a credit-card balance, you’ll want to pay it down as quickly as possible. Start by tracking all of your balances while being mindful of interest rates and hidden fees. Next, optimize your repayments by paying off any high-interest debt first and/or taking advantage of a debt consolidation/refinancing program.

4. Protect yourself. When it comes to insurance coverage, are you adequately protected? Having the appropriate amount of insurance to help protect yourself against possible losses is an important part of any financial strategy. Your insurance needs will depend on your individual circumstances and can change over time. As a result, you’ll want to make sure your coverage properly aligns with your income and family/personal circumstances.

12020 Survey of the States, Council for Economic Education

Prepared by Broadridge Advisor Solutions Copyright 2022.