How would you rate this content?

This year has been challenging on many fronts, but one financial opportunity may have emerged from the economic turbulence. If you’ve been thinking about converting your traditional IRA to a Roth, now might be an appropriate time to do so.

Conversion Basics

Roth IRAs offer tax-free income in retirement. Contributions to a Roth IRA are not tax-deductible, but qualified withdrawals, including any earnings, are free of federal income tax. Such withdrawals may also be free of any state income tax that would apply to retirement plan distributions.

Generally, a Roth distribution is considered “qualified” if it meets a five-year holding requirement and you are age 59½ or older, become permanently disabled, or die (other exceptions may apply).

Regardless of your filing status or how much you earn, you can convert assets in a traditional IRA to a Roth IRA. Though annual IRA contribution limits are relatively low ($6,000 to all IRAs combined in 2020, or $7,000 if you are age 50 or older), there is no limit to the amount you can convert or the number of conversions you can make during a calendar year. An inherited traditional IRA cannot be converted to a Roth, but a spouse beneficiary who treats an inherited IRA as his or her own can convert the assets.

Converted assets are subject to federal income tax in the year of conversion and may also be subject to state taxes. This could result in a substantial tax bill, depending on the value of your account, and could move you into a higher tax bracket. However, if all conditions are met, the Roth account will incur no further income tax liability and you won’t be subject to required minimum distributions. (Designated beneficiaries are required to take withdrawals based on certain rules and time frames, depending on their age and relationship to the original account holder, but such withdrawals would be free of federal tax.)

Why Now?

Comparatively low income tax rates combined with the impact of the economic downturn might make this an appropriate time to consider a Roth conversion.

The lower income tax rates passed in 2017 are scheduled to expire at year-end 2025; however, some industry observers have noted that taxes may rise even sooner due to rising deficits exacerbated by the pandemic relief measures.

Moreover, if the value of your IRA remains below its pre-pandemic value, the tax obligation on your conversion will be lower than if you had converted prior to the downturn. If your income is lower in 2020 due to the economic challenges, your tax rate could be lower as well.

Any or all of these factors may make it worth considering a Roth conversion, provided you have the funds available to cover the tax obligation.

As long as your traditional and Roth IRAs are with the same provider, you can typically transfer shares from one account to the other. When share prices are lower, as they may be in the current market environment, you could theoretically convert more shares for each dollar and would have more shares in your Roth account to pursue tax-free growth. Of course, there is also a risk that the converted assets will go down in value.

Using Conversions to Make “Annual Contributions”

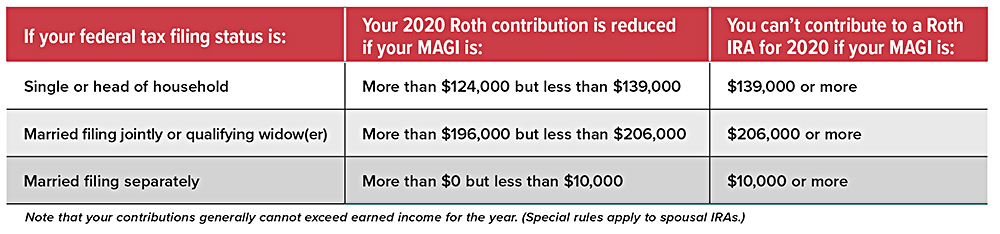

Finally, if you are not eligible to contribute to a Roth IRA because your modified adjusted gross income (MAGI) is too high (see table), a Roth conversion may offer a workaround. You can make nondeductible contributions to a traditional IRA and then convert traditional IRA assets to a Roth. This is often called a “back-door” Roth IRA.

As this history-making year approaches its end, this is a good time to think about last-minute moves that might benefit your financial and tax situation. A Roth conversion could be an appropriate strategy.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Prepared by Broadridge Advisor Solutions Copyright 2020.

How would you rate this content?

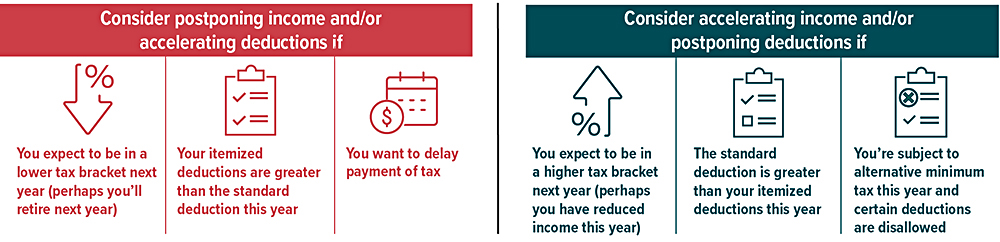

Here are some things to consider as you weigh potential tax moves before the end of the year.

Defer income to next year

Consider opportunities to defer income to 2021, particularly if you think you may be in a lower tax bracket then. For example, you may be able to defer a year-end bonus or delay the collection of business debts, rents, and payments for services in order to postpone payment of tax on the income until next year.

Accelerate deductions

Look for opportunities to accelerate deductions into the current tax year. If you itemize deductions, making payments for deductible expenses such as medical expenses, qualifying interest, and state taxes before the end of the year (instead of paying them in early 2021) could make a difference on your 2020 return.

Make deductible charitable contributions

If you itemize deductions on your federal income tax return, you can generally deduct charitable contributions, but the deduction is limited to 60%, 30%, or 20% of your adjusted gross income (AGI), depending on the type of property that you give and the type of organization to which you contribute. (Excess amounts can be carried over for up to five years.) For 2020 charitable gifts, the normal rules have been enhanced: The limit is increased to 100% of AGI for direct cash gifts to public charities. And even if you don’t itemize deductions, you can receive a $300 charitable deduction for direct cash gifts to public charities (in addition to the standard deduction).

Bump up withholding

If it looks as though you’re going to owe federal income tax for the year, consider increasing your withholding on Form W-4 for the remainder of the year to cover the shortfall. The biggest advantage in doing so is that withholding is considered as having been paid evenly throughout the year instead of when the dollars are actually taken from your paycheck.

More to Consider

Here are some other things you may want to consider as part of your year-end tax review.

Maximize retirement savings

Deductible contributions to a traditional IRA and pre-tax contributions to an employer-sponsored retirement plan such as a 401(k) can reduce your 2020 taxable income. If you haven’t already contributed up to the maximum amount allowed, consider doing so. For 2020, you can contribute up to $19,500 to a 401(k) plan ($26,000 if you’re age 50 or older) and up to $6,000 to traditional and Roth* IRAs combined ($7,000 if you’re age 50 or older). The window to make 2020 contributions to an employer plan generally closes at the end of the year, while you have until April 15, 2021, to make 2020 IRA contributions. (*Roth contributions are not deductible, but Roth qualified distributions are not taxable.)

Avoid RMDs in 2020

Normally, once you reach age 70½ (age 72 if you reach age 70½ after 2019), you generally must start taking required minimum distributions (RMDs) from traditional IRAs and employer-sponsored retirement plans. Distributions are also generally required to beneficiaries after the death of the IRA owner or plan participant. However, recent legislation has waived RMDs from IRAs and most employer retirement plans for 2020 and you don’t have to take such distributions. If you have already taken a distribution for 2020 that is not required, you may be able to roll it over to an eligible retirement plan.

Weigh year-end investment moves

Though you shouldn’t let tax considerations drive your investment decisions, it’s worth considering the tax implications of any year-end investment moves. For example, if you have realized net capital gains from selling securities at a profit, you might avoid being taxed on some or all of those gains by selling losing positions. Any losses above the amount of your gains can be used to offset up to $3,000 of ordinary income ($1,500 if your filing status is married filing separately) or carried forward to reduce your taxes in future years.

Prepared by Broadridge Advisor Solutions Copyright 2020.

How would you rate this content?

During the holiday shopping season, your credit score is probably the last thing on your mind. But as you start your seasonal spending, remember to use credit wisely so you can start the new year with a healthy credit score. The following tips can help you maintain or potentially improve your credit score throughout the holidays and beyond.

Know how your credit score is calculated. The most common credit score is expressed as a three-digit number ranging from 300 to 850. (Some lenders may calculate it differently, but this should be a good guideline.) The score is derived from a formula using five weighted factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and types of credit in use (10%).1 Keeping these components in mind can help you stay on track with your credit.

Make payments on time. Set up alerts for every credit card you have so you don’t miss notifications of charges, statements, or due dates. To help avoid missed payments, set up automatic payments. If you do miss a payment, contact the lender and bring the account up-to-date as soon as possible.

Keep credit-card balances low. If you carry a balance, consider paying down the cards with the highest balance-to-credit limit ratio first while keeping up minimum (or higher) payments on others. Don’t “max out” your available credit.

Be careful about opening and closing accounts. Some retailers may offer discounts on purchases if you sign up for a store credit card, but store cards often have high interest rates and low credit limits. Unless you plan on shopping regularly at that store and the card offers useful bonuses or discounts, avoid applying for new credit cards solely to save money on purchases. Likewise, try not to close multiple accounts within a short period of time — this could actually hurt your credit score.

Research before using credit boosting services. You might be tempted to sign up for a free service that promises to instantly boost your credit score, but they’re usually only worth considering if you have a thin credit file and/or a low credit score. These services can’t fix any late payments you’ve made or reduce the impact of an excessive level of debt.

Monitor your credit report regularly. You can order a free credit report annually* from each of the three major consumer reporting agencies at annualcreditreport.com. If you find incorrect information on your credit report, contact the reporting agency in writing, provide copies of any corroborating documents, and ask for an investigation.

*Due to the COVID-19 pandemic, Equifax, Experian, and TransUnion are offering free weekly online reports through April 2021.

Prepared by Broadridge Advisor Solutions Copyright 2020.

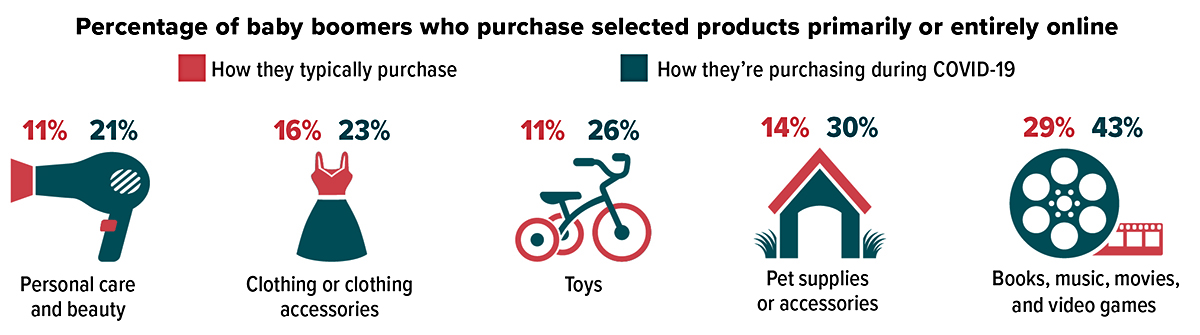

The coronavirus pandemic has forced consumers to change many habits, including how they shop. This is particularly true for baby boomers (ages 56 to 74). Nearly half (45%) said they shop online more, with some product categories seeing a large shift in online purchases.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

The longest bull market in history lasted almost 11 years before coronavirus fears and the realities of a seriously disrupted U.S. economy brought it to an end.1

Bear markets are typically defined as declines of 20% or more from the most recent high, and bull markets are sustained increases of 20% or more from the bear market low. But there is no official declaration, so often there are different interpretations and a fair amount of debate regarding when these cycles begin and end.

Between February 19 and March 23, 2020, the S&P 500 fell 34% and then took just 15 days to bounce back above the 20% threshold that would technically mark the beginning of a new bull market.2

Still, most investors wait to see if volatility subsides and higher prices persist before they cheer the exit of a bear market. And in the midst of the pandemic, without a clear economic picture, it could be more difficult than usual to tell whether any market advance is a short-term rally or the start of a longer upward trend.

Historical Perspective

The CBOE Volatility Index (VIX), a closely watched measure of stock market volatility and investor anxiety, hit all-time highs in March 2020.3

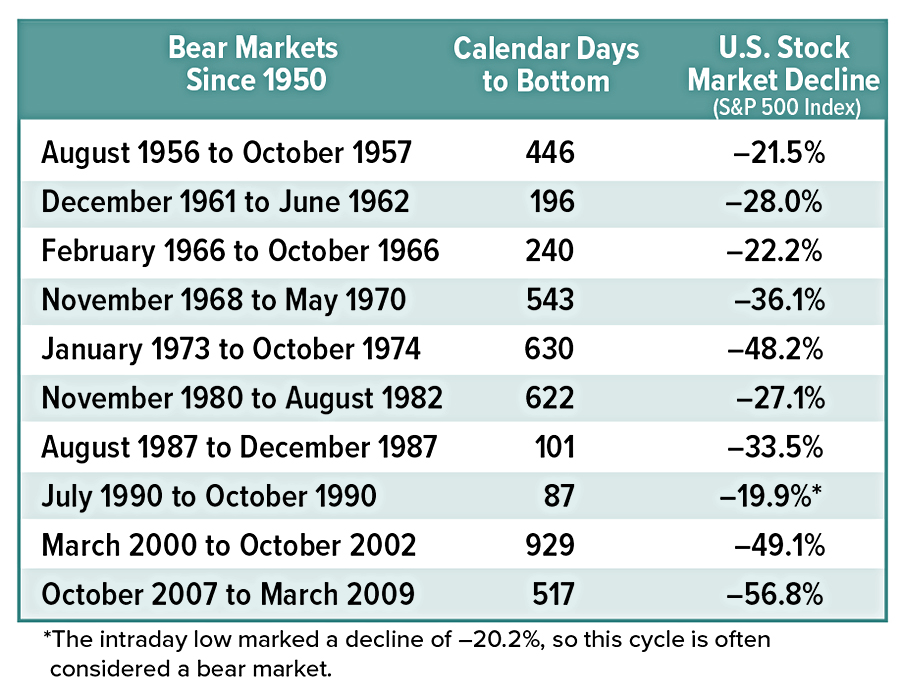

If you are losing sleep over volatility driven by disheartening news, it may help to remember that the economy and the stock market are cyclical. There have been 10 bear markets since 1950 (not counting the one that began in 2020). Each of these declines was triggered by a different set of circumstances, but the market recovered eventually every time (see table). 4

On average, bull markets lasted longer (1,955 days) than bear markets (431 days) over this period, and the average bull market advance (172.0%) was greater than the average bear market decline (-34.2%).

The bottom line is that neither the ups nor the downs last forever, even if they feel as though they will. There are buying opportunities in the midst of the worst downturns. And in some cases, people have profited over time by investing carefully just when things seemed bleakest.

Making Changes

If you’re reconsidering your current investment strategy, a volatile market is probably the worst time to turn your portfolio inside out. Dramatic price swings can magnify the impact of a wholesale restructuring if the timing of that move is a little off.

Changes in your portfolio don’t necessarily need to happen all at once. Having appropriate asset allocation and diversification is still the fundamental basis of thoughtful investment planning, so try not to let fear derail your long-term goals.

The return and principal value of stocks fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. Asset allocation and diversification are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.

The S&P 500 is an unmanaged group of securities that is considered to be representative of the U.S. stock market in general. The performance of an unmanaged index is not indicative of the performance of any specific investment. Individuals cannot invest directly in an index. Past performance is not a guarantee of future results. Actual results will vary.1-2,4) Yahoo! Finance, 2020 (data for the period 6/13/1949 to 4/7/2020)

3) MarketWatch, March 31, 2020

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020