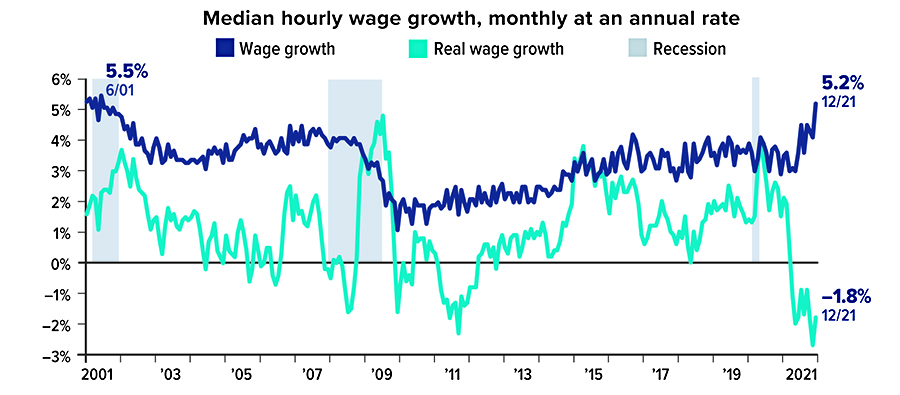

Driven by labor shortages, median hourly wages increased at an annual rate of 5.2% in December 2021, the highest level since June 2001. However, inflation cuts into buying power, and real wages — adjusted for inflation — actually dropped as inflation spiked in 2021. By contrast, negative inflation (deflation) during the Great Recession sent real wages skyrocketing temporarily even as non-adjusted wage growth declined.

Sources: Federal Reserve Bank of Atlanta, 2022, and U.S. Bureau of Labor Statistics, 2022, data 1/2001 to 12/2021. (Wage growth is calculated by comparing the median percentage change in wages reported by individuals 12 months apart; real wage growth is calculated by subtracting CPI-U inflation from wage growth.)

Prepared by Broadridge Advisor Solutions Copyright 2022.