By now you know that Congress has passed a $2 trillion relief bill to help keep individuals and businesses afloat during these difficult times. The Coronavirus Aid, Relief, and Economic Security (CARES) Act contains many provisions. Here are five that may benefit you or your business.

1. Recovery Rebates

Many Americans will receive a one-time cash payment of $1,200. Each U.S. resident or citizen with an adjusted gross income (AGI) under $75,000 ($112,500 for heads of household and $150,000 for married couples filing a joint return) who is not the dependent of another taxpayer and has a work-eligible Social Security number, may receive the full rebate. Parents may also receive an additional $500 per dependent child under the age of 17.

The $1,200 rebate amount will decrease by $5 for every $100 in excess of the AGI thresholds until it completely phases out. For example, the $1,200 rebate completely phases out at an AGI of $99,000 for an individual taxpayer and the $2,400 rebate phases out at $198,000 for a married couple filing a joint return.

Rebate payments will be based on 2019 income tax returns (2018 if no 2019 return was filed) and will be sent by the IRS via direct deposit or mail. Eligible individuals who receive Social Security benefits but don’t file tax returns will also receive these payments, based on information provided by the Social Security Administration.

The rebate is not taxable. Because the rebate is actually an advance on a refundable tax credit against 2020 taxes, someone who didn’t qualify for the rebate based on 2018 or 2019 income might still receive a full or partial rebate when filing a 2020 tax return.

2. Extra Unemployment Benefits

The federal government will provide $600 per week to those who are eligible for unemployment benefits as a result of COVID-19, on top of any state unemployment benefits an individual receives. Unemployed individuals may qualify for this additional benefit for up to four months (through July 31.) The federal government will also fund up to an additional 13 weeks of unemployment benefits for those who have exhausted their state benefits (up to 39 weeks of benefits) through the end of 2020.

The CARES Act also provides assistance to workers who have been affected by the COVID-19 pandemic but who normally wouldn’t be eligible for unemployment benefits, including self-employed individuals, part-time workers, freelancers, independent contractors, and gig workers. Individuals who have to leave work for coronavirus-related reasons are also potentially eligible for benefits.

3. Federal Student Loan Deferrals

For all borrowers of federal student loans, payments of principal and interest will be automatically suspended for six months, through September 30, without penalty to the borrower. Federal student loans include Direct Loans (which includes PLUS Loans), as well as Federal Perkins Loans and Federal Family Education Loan (FFEL) Program loans held by the Department of Education. Private student loans are not eligible.

4. IRA and Retirement Plan Distributions

Required minimum distributions from IRAs and employer-sponsored retirement plans will not apply for the 2020 calendar year. In addition, the 10% premature distribution penalty tax that would normally apply for distributions made prior to age 59½ (unless an exception applied) is waived for coronavirus-related retirement plan distributions of up to $100,000. The tax obligation may be spread over three years, with up to three years to reinvest the money.

5. Help for Businesses

The CARES Act includes several provisions designed to help self-employed individuals and small businesses weather the financial impact of the COVID-19 crisis.

Self-employed individuals and small businesses with fewer than 500 employees may apply for a Paycheck Protection Loan through a Small Business Association (SBA) lender. Businesses may borrow up to 2.5 times their average monthly payroll costs, up to $10 million. This loan may be forgiven if an employer continues paying employees during the eight weeks following the origination of the loan and uses the money for payroll costs (including health benefits), rent or mortgage interest, and utility costs.

Also available are emergency grants of up to $10,000 (that do not need to be repaid if certain conditions are met), SBA disaster loans, and relief for business owners with existing SBA loans.

Businesses of all sizes may qualify for a refundable payroll tax credit of 50% of wages paid to employees during the crisis, up to $10,000 per employee. The credit is applied against the employer’s share of Social Security payroll taxes.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

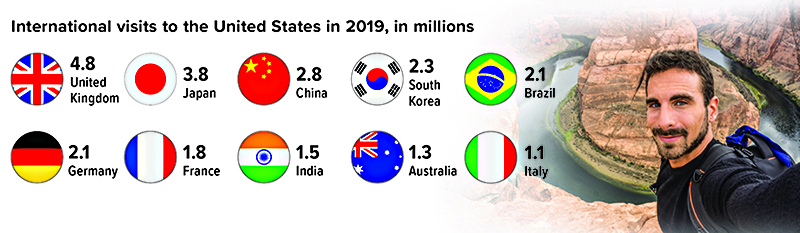

More than 79 million foreign tourists visited the United States in 2019, adding $254 billion to the U.S. economy. Residents of Canada and Mexico accounted for almost half of the total, while the countries below were the top 10 sources of overseas visitors. Travel restrictions and lockdowns due to COVID-19 have severely disrupted the flow of foreign tourists in 2020. It’s too early to know the full extent of the damage to the tourism sector, but the effects may continue for some time after the virus is controlled.

Source: National Travel and Tourism Office, 2020

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

Would you take on a 30-day challenge to spend money only on necessities such as rent, utilities, and groceries? During a no-spend month, many common activities — including dining out, buying movie or concert tickets, and shopping for clothes — are avoided at all costs.

The idea behind a 30-day challenge is that the time period is just long enough to help change bad habits without seeming intolerable. If frugality isn’t normally your forte, closely scrutinizing your spending could reap hundreds of dollars in savings. More important, it could help identify ways you might be wasting money on a regular basis.

Start by setting a positive goal for the money. Will you use the extra savings to pay down credit card debt or build up your emergency fund?

Here are some other ways to prepare for a successful challenge.

Time it right. Periods that include major holidays, planned vacations from work, and family birthdays are probably not the best for taking on this type of household experiment. On the other hand, it could be ideal to begin the new year with a “fiscal fast.”

Establish rules. Take your fixed expenses (i.e., rent/mortgage, utilities, phone bill, insurance payments) into account when planning your no-spend month. Evaluate your typical monthly discretionary spending to figure out where you can reduce or eliminate your spending for the month.

Plan to break patterns. Fill up your freezer and pantry with groceries and collect ideas for easy homemade meals. Steer clear of your personal spending triggers, which could mean staying off the Internet or waiting until later to meet up with friends who are big spenders.

Seek out free and fun entertainment. You don’t have to stay home for an entire month. Spend the day visiting a public park or beach, or look for free concerts, outdoor movies, art festivals, workshops, and other special events hosted by community groups.

Stay focused. When you get tempted to spend, remember your goal for the money you’ve saved. Keep a record of your progress to have a tangible reminder that your efforts will pay off.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

According to a recent survey, 76% of Americans reported having at least one financial regret. Over half of this group said it had to do with savings: 27% didn’t start saving for retirement soon enough, 19% didn’t contribute enough to an emergency fund, and 10% wish they had saved more for college.1

The saving conundrum

What’s preventing Americans from saving more? It’s a confluence of factors: stagnant wages over many years; the high cost of housing and college; meeting everyday expenses for food, utilities, and child care; and squeezing in unpredictable expenses for things like health care, car maintenance, and home repairs. When expenses are too high, people can’t save, and they often must borrow to buy what they need or want, which can lead to a never-ending cycle of debt.

People make financial decisions all the time, and sometimes these decisions don’t pan out as intended. Hindsight is 20/20, of course. Looking back, would you change anything?

Paying too much for housing

Are housing costs straining your budget? A standard lender guideline is to allocate no more than 28% of your income toward housing expenses, including your monthly mortgage payment, real estate taxes, homeowners insurance, and association dues (the “front-end” ratio), and no more than 36% of your income to cover all your monthly debt obligations, including housing expenses plus credit card bills, student loans, car loans, child support, and any other debt that shows on your credit report and requires monthly payments (the “back-end” ratio).

But just because a lender determines how much you can afford to borrow doesn’t mean you should. Why not set your ratios lower? Many things can throw off your ability to pay your monthly mortgage bill down the road — a job loss, one spouse giving up a job to take care of children, an unexpected medical expense, tuition bills for you or your child.

Potential solutions: To lower your housing costs, consider downsizing to a smaller home (or apartment) in the same area, researching and moving to a less expensive town or state, or renting out a portion of your current home. In addition, watch interest rates and refinance when the numbers make sense.

Paying too much for college

Outstanding student debt levels in the United States are off the charts, and it’s not just students who are borrowing. Approximately 15 million student loan borrowers are age 40 and older, and this demographic accounts for almost 40% of all student loan debt.2

Potential solutions: If you have a child in college now, ask the financial aid office about the availability of college-sponsored scholarships for current students, or consider having your child transfer to a less expensive school. If you have a child who is about to go to college, run the net price calculator that’s available on every college’s website to get an estimate of what your out-of-pocket costs will be at that school. Look at state universities or community colleges, which tend to be the most affordable. For any school, understand exactly how much you and/or your child will need to borrow — and what the monthly loan payment will be after graduation — before signing any loan documents.

Paying too much for your car

Automobile prices have grown rapidly in the last decade, and most drivers borrow to pay for their cars, with seven-year loans becoming more common.3 As a result, a growing number of buyers won’t pay off their auto loans before they trade in their cars for a new one, creating a cycle of debt.

Potential solutions: Consider buying a used car instead of a new one, be proactive with maintenance and tuneups, and try to use public transportation when possible to prolong the life of your car. As with your home, watch interest rates and refinance when the numbers make sense.

Keeping up with the Joneses

It’s easy to want what your friends, colleagues, or neighbors have — nice cars, trips, home amenities, memberships — and spend money (and possibly go into debt) to get them. That’s a mistake. Live within your means, not someone else’s.

Potential solutions: Aim to save at least 10% of your current income for retirement and try to set aside a few thousand dollars for an emergency fund (three to six months’ worth of monthly expenses is a common guideline). If you can’t do that, cut back on discretionary items, look for ways to lower your fixed costs, or explore ways to increase your current income.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

Losing a loved one can be a difficult experience. Despite the emotional trauma involved, you may also be responsible for handling a variety of financial, legal, and administrative tasks. You may find yourself unsure of where to begin and what to do.

However, do not be hasty when settling your loved one’s estate. Important decisions need to be made regarding distributions, which must be made in compliance with the will and applicable laws. Seek an experienced estate planning professional for advice. The following suggestions may provide a roadmap to help you navigate through the process.

Initial tasks

Note: Some of the following tasks may have to be completed by the estate’s personal representative.

•Upon the death of your loved one, call close family members, friends, and clergy first because you’ll need their emotional support.

•Arrange the funeral, burial or cremation, and memorial service. Hopefully, your loved one will have made arrangements ahead of time. Then notify family and friends of the final arrangements and place an obituary in the local paper (often the funeral home will handle this for you).

•Obtain certified copies of the death certificate (again, the funeral home should be able to get copies for you).

•Find and review your family member’s finances, and look for relevant documents such as a will and trusts, deeds and titles to motor vehicles.

•Report the death to Social Security. If your loved one was receiving benefits via direct deposit, request that the bank return funds received for the month of death and thereafter to Social Security. Do not cash any Social Security checks received by mail. Return all checks to Social Security as soon as possible.

•Make a list of assets and debts. Be on the lookout for pension plans, IRA, 401(k), and other retirement plans owned by the deceased, as well as life insurance policies, bank accounts, and investments. Notify those named as beneficiaries of assets such as life insurance and retirement plans.

•Make sure mortgage and insurance payments continue to be made while the estate is being settled.

•Contact all credit card companies and let them know of the death. Cancel all cards unless you’re named on the account and wish to retain the card.

Within 1 to 3 months of death

•File the will with the appropriate probate court. If real estate was owned out of state, file ancillary probate in that state. If there is no will, contact the probate court for instructions or contact a probate attorney for assistance.

•Notify creditors by mail and by placing a notice in the newspaper. Claims must be made within the statute of limitations, which varies from state to state (30 days from actual notice is common). Insist on proof of all claims. Notify heirs named in the will. Often, the probate process will require formal notification to heirs and others named in the will.

Within 6 to 9 months of death

•Federal and/or state estate tax return(s) may need to be filed, usually within nine months of death, although state laws may vary.

•Also, federal and state income taxes are due for the year of death on the normal filing date, unless an extension is requested. If there are trusts, separate income tax returns may be necessary.

•Update your own estate plan if your loved one was a beneficiary or appointed as an agent, trustee, or guardian.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020