“London Bridge is down.” On September 8, 2022, those words were reportedly used to launch what were arguably the most complex end-of-life proceedings the world had ever witnessed: the funeral arrangements for Queen Elizabeth II. The plan, known as Operation London Bridge, laid out in exacting detail how the ensuing days would unfold. Although most families don’t need a playbook as intricate as the royals, a comprehensive end-of-life plan can significantly ease the burden on family members during a highly emotional period.

Guidance in a Medical Crisis

What would happen if you became incapacitated and could not make financial or medical decisions for yourself? To help ensure that your affairs continue to be managed by someone you trust and according to your wishes, you might consider creating a durable power of attorney (DPOA) and an advance medical directive.

A DPOA authorizes someone to manage your finances on your behalf, while a medical directive documents your wishes for medical care, such as whether you want extraordinary measures to prolong life if there is no chance of recovery. There are several types of DPOAs and advance medical directives; each has its own purpose, benefits, and drawbacks and may not be effective in some states.

Funeral Instructions

Planning your funeral or similar commemoration can relieve significant stress on your family members. Decisions would typically cover whether you want a burial or cremation, a wake with or without viewing, a religious ceremony or secular event, and could include details such as music, readings, speakers/clergy, flowers, venues, and an obituary. You might discuss thoughts with family members, taking their ideas into consideration. You might also consult a trusted funeral director who can help you navigate the various options, decide whether to prepay for arrangements, and become a valuable resource to your family when the time comes.

Estate Management

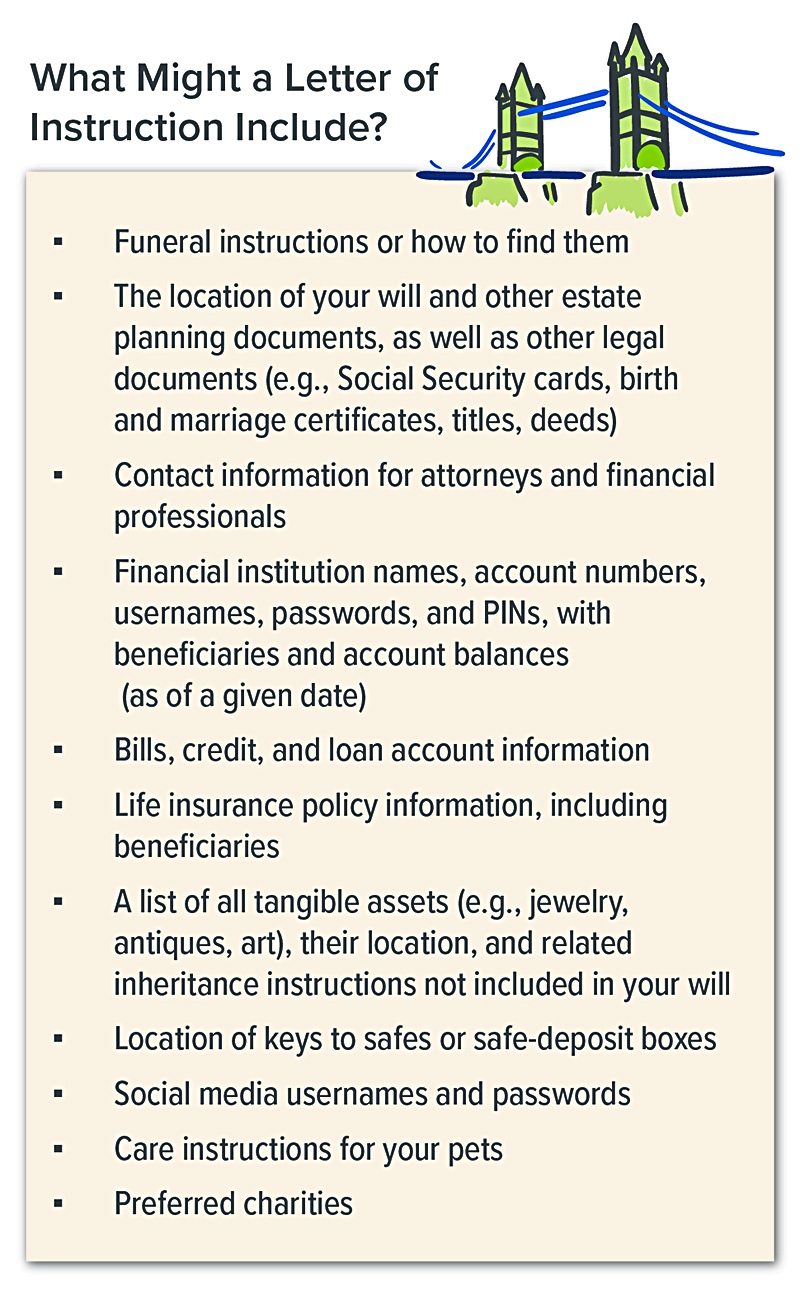

The most fundamental components of an estate plan are also among the most important: a will and a letter of instruction.

A will states how you wish to disburse your assets, names an executor to act as your legal representative, provides guidance for the management of your financial affairs, and (if appropriate) identifies who you want to be guardian of your minor children and their assets. A letter of instruction has no legal status but provides vital details that complement your will (see graphic).

You might also familiarize yourself with the death-related tax rules at both the federal and state levels. The 2023 federal estate tax exemption is $12.92 million. Although that sounds like a lot, 17 states impose their own estate and/or inheritance tax — most at much lower thresholds. When you consider that an estate includes the value of your home, insurance policies, retirement plans, and other assets, it may be easier than you’d expect to trigger a taxable situation. (Estate tax is imposed on the estate of the deceased, while an inheritance tax is imposed on the beneficiary.)

Seek Assistance

For more information on how to create your own Operation London Bridge, contact an estate planning attorney. Once your plan is established, store all documents in a safe place and communicate its location to your executor.

Prepared by Broadridge Advisor Solutions Copyright 2023.

Recent research from the U.S. Department of Health and Human Services suggests that most Americans turning age 65 will need long-term care support during their lifetimes.¹

If the need arises, how will you handle potential long-term care for yourself or a loved one? Planning for the consequences of aging in general, and long-term care in particular, will depend on your preferences and circumstances. A long-term care plan should account for the different types of care you may need and the different settings in which you might receive that care. These are the most common options.

Your Home

Given a choice, you might prefer to receive long-term care support in your own home. Family caregivers, friends, or trained homemakers could provide assistance with everyday tasks, and professionals such as nurses and home health aides could provide home health care. In addition, a variety of community support services may be available, including adult day-care centers and transportation services. In any case, receiving care at home offers a measure of independence in a familiar environment.

Community Care Retirement Communities (CCRCs)

Also known as life plan communities, CCRCs provide a range of services — from independent living to full-time skilled nursing care — all in the same location, allowing you to age in place. Most CCRCs combine housing options at one location and may include townhouses or cottages for independent living, assisted living apartments, and nursing home accommodations.

Assisted Living Facilities

If you want to remain independent but need some assistance with activities of daily living, you might choose to live in an assisted living facility. These home-like facilities offer housing, meals, and personal care services, but generally not medical or nursing services.

Nursing Homes

People who enter a nursing home usually have a disabling condition or cognitive disorder and can no longer take care of themselves. State-licensed nursing facilities offer more specialized skilled care, intermediate care, and custodial care. This is the most expensive way to receive long-term care.

Take some time to think about what the future might hold. Planning ahead can help ensure that you receive the type of care you need, in the setting that you prefer, as you grow older.1) U.S. Department of Health and Human Services, 2021

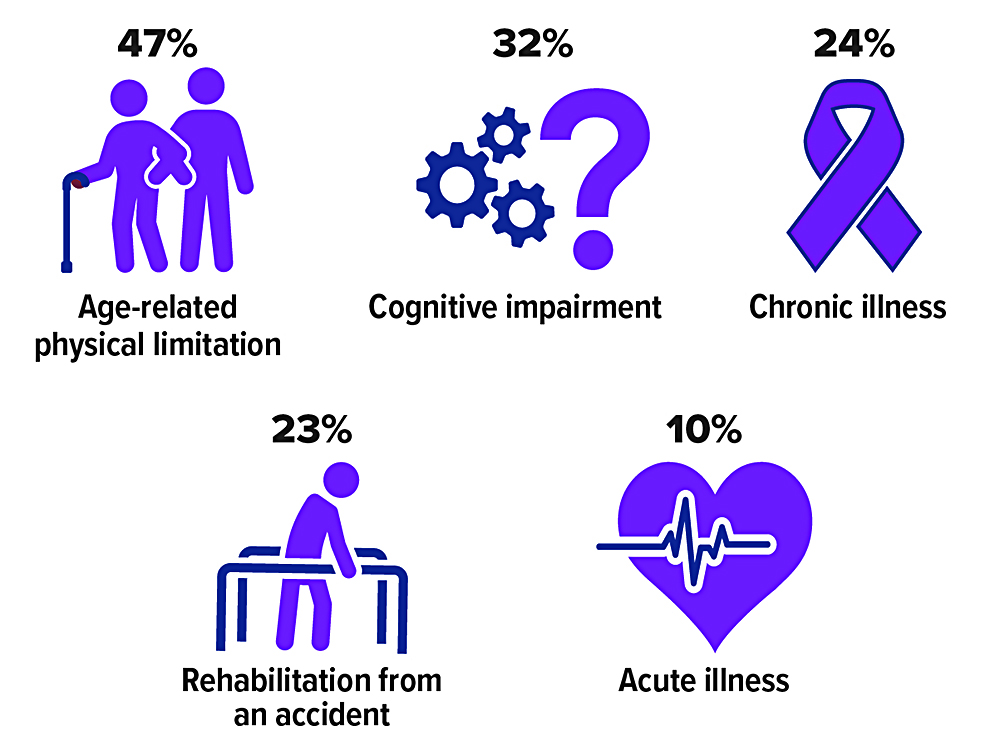

Reasons for Care

A 65-year-old has a nearly 70% chance of needing long-term care support and services at some point. The average length of long-term care in 2021 was 3.5 years, up from 3 years in 2018. People need care for a variety of reasons, but the most common is simply the physical limitations of aging.

Source: Genworth, 2021 (multiple responses allowed)

Prepared by Broadridge Advisor Solutions Copyright 2023.

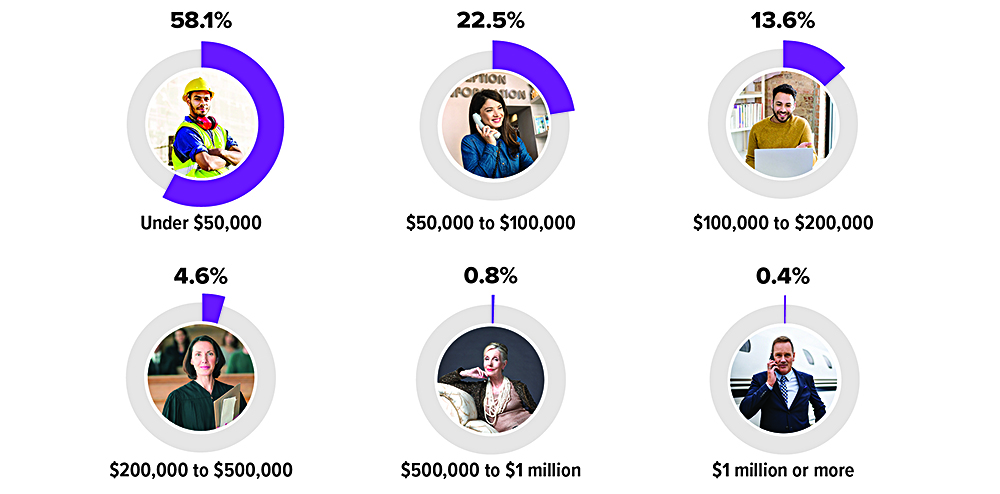

The IRS processed more than 164 million individual income tax returns for tax year 2020 (most recent full-year data). Almost three out of five returns showed an adjusted gross income (AGI) under $50,000, while a little over 1% showed an AGI of $500,000 or more.

Source: Internal Revenue Service, 2022

Prepared by Broadridge Advisor Solutions Copyright 2023.

Over time, finances tend to get complicated, especially when you’re juggling multiple goals and accounts. Simplifying your finances requires a bit of effort up front, but making just a few changes may help free up more time to focus on your financial priorities.

Make Saving Automatic

Saving for a goal is simpler when money is set aside automatically. For example, you may be able to regularly and automatically deposit a portion of your paycheck into a retirement account through your employer. Your contribution level may also increase automatically each year, if your plan offers this feature. Employers may also allow you to split your direct deposit into multiple accounts, enabling you to build up a college fund or an emergency fund, or direct money to an investment account.

Another way to make saving for multiple goals easier is to set up recurring transfers between your savings, checking, or other financial accounts. You decide on the frequency and timing of those transfers, and you can quickly make necessary adjustments.

Consolidate Retirement Funds

If you’ve had a few jobs, you might have several retirement accounts, such as IRAs and 401(k) or 403(b) plans, with current and past employers. Consolidating them in one place may help make it easier to monitor and manage your retirement savings and distributions, and prevent you (or your beneficiaries) from forgetting about older or lower-balance accounts. Not all accounts can be combined, and there may be tax consequences, so discuss your options with your financial and/or tax professionals.

Take a Credit Card Inventory

Credit cards are convenient, but managing multiple credit-card accounts can be time-consuming and costly. Losing track of balances and due dates may lead to increased interest charges or late payments. You could also miss out on some of the rewards and benefits your cards offer. If you’ve accumulated a few credit cards, review interest rates, terms, credit limits, and benefits that may have changed since you got the cards. Ordering a copy of your credit report can help you quickly see all of your open credit-card accounts — there may be some you’ve forgotten about. Visit annualcreditreport.com to get a free credit report from each of the three major credit reporting agencies (Experian, Equifax, and TransUnion).

Once you know what you have, you can decide which cards to use and put the rest aside. Because it’s possible that your credit score might take a temporary hit, it may not always be a good idea to close accounts you’re not using unless you have a compelling reason, such as a high annual fee or exposure to fraud.

Prepared by Broadridge Advisor Solutions Copyright 2023.

Maintaining an appropriate balance of stocks and bonds is one of the most fundamental concepts in constructing an investment portfolio. Stocks provide greater growth potential with higher risk and relatively low income; bonds tend to be more stable, with modest potential for growth and higher income. Together, they may result in a less volatile portfolio that might not grow as fast as a stock-only portfolio during a rising market, but may not lose as much during a market downturn.

Three Objectives

Balanced mutual funds attempt to follow a similar strategy. The fund manager typically strives for a specific mix, such as 60% stocks and 40% bonds, but the balance might vary within limits spelled out in the prospectus. These funds generally have three objectives: conserve principal, provide income, and pursue long-term growth. Of course, there is no guarantee that a fund will meet its objectives.

When investing in a balanced fund, you should consider the fund’s asset mix, objectives, and the rebalancing guidelines as the asset mix changes due to market performance. The fund manager may rebalance to keep a balanced fund on track, but this could create a taxable event for investors if the fund is not held in a tax-deferred account.

Core Holding

Unlike “funds of funds,” which hold a variety of broad-based funds and are often meant to be an investor’s only holding, balanced funds typically include individual stocks and bonds. They are generally not intended to be the only investment in a portfolio, because they might not be sufficiently diversified. Instead, a balanced fund could be a core holding that enables you to pursue diversification and other goals through a wider range of investments.

You may want to invest in other asset classes, hold a wider variety of individual securities, and/or add funds that focus on different types of stocks or bonds than those in the balanced fund. And you might want to pursue an asset allocation strategy that differs from the allocation in the fund. For example, holding 60% stocks and 40% bonds in a portfolio might be too conservative for a younger investor and too aggressive for a retired investor, but a balanced fund with that allocation could play an important role in the portfolio of either investor.

Heavier on Stocks or Bonds?

Balanced funds typically hold a larger percentage of stocks than bonds, but some take a more conservative approach and hold a larger percentage of bonds. Depending on your situation and risk tolerance, you might consider holding more than one balanced fund, one tilted toward stocks and the other tilted toward bonds. This could be helpful in tweaking your overall asset allocation. For example, you may invest more heavily in a stock-focused balanced fund while you are working and shift more assets to a bond-focused fund as you approach retirement.

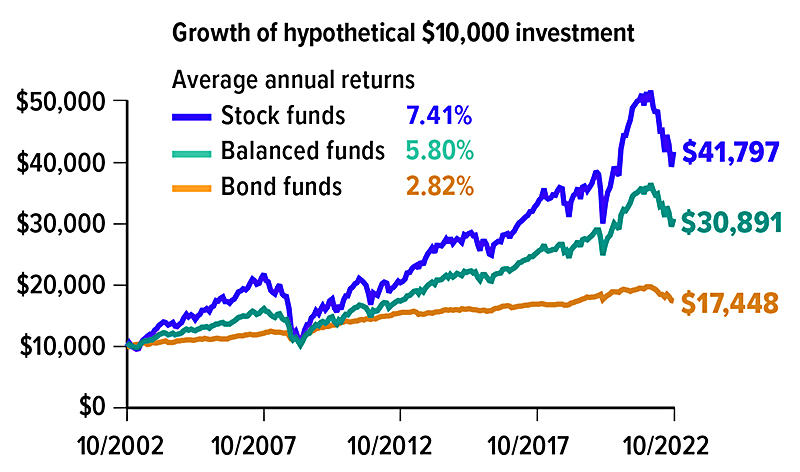

Lower Highs, Higher Lows

During the 20-year period ending in October 2022, balanced funds were less volatile than stock funds, while producing higher returns than bond funds.

Keep in mind that as you change the asset allocation and diversification of your portfolio, you may also be changing the level of risk. Asset allocation and diversification are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.

The return and principal value of all investments fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. Bond funds, including balanced funds, are subject to the same inflation, interest-rate, and credit risks associated with their underlying bonds. As interest rates rise, bond prices typically fall, which can adversely affect a bond fund’s performance.

Mutual funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. You should read the prospectus carefully before investing.

Prepared by Broadridge Advisor Solutions Copyright 2023.